By Jarred Mailer-Lyons, Head of Digital at The MediaShop

The paranoia is real and if you’re worried about your devices listening in to your conversations and tracking your every move then it’s time to disable, de-activate and delete…

I was recently interviewed on East Coast Radio (ECR) about our phones tracking every move we make, the conversations we have and actions we take. While we don’t know exactly what data is stored, shared and used by some of the global tech giants – we do know that consumer data is core to their multibillion dollar services they offer to market.

I was recently interviewed on East Coast Radio (ECR) about our phones tracking every move we make, the conversations we have and actions we take. While we don’t know exactly what data is stored, shared and used by some of the global tech giants – we do know that consumer data is core to their multibillion dollar services they offer to market.

Now when I talk about deactivating and disabling – I’m specifically referring to voice assistants, otherwise you may as well be living back in the arc ages as most of the devices and apps we use today collect some form of data in order to provide their users with the best possible experience. But have you ever noticed relevant ads emerging on sites after mentioning something in a conversation? Like that time you were chatting to your significant other about a quick getaway over the long weekend and then ‘suddenly’ started seeing ads of accommodation, car rentals and cheap flights? Or when you were considering buying a new car and then were immediately bombarded with ads for car enthusiasts and deals on the latest versions? Is it mind boggling and just a coincidence, like when you’ve noticed a car you’re interested in and then suddenly see every second person has one on the road or, are our phones actually listening in on our conversations?

So the real question is, are our phones allowed to be tracking literally everything we say and do?

Firstly, you need to start thinking about more than just your mobile phone collecting your data or listening in on your conversations. If of course if you are concerned, it’s important for you to recognise just how many different kinds of sensors you have allowed into your home and office that are constantly collecting this data and listening in.

By taking a deeper look at Google’s policies and some research and methodologies around data collection, we can start understanding how and why it is collected and of course their policy around sharing this data over to third parties.

We use Google suite of tools so often that it’s almost hard to think of as a set of products and services. According to the 2021 SA Hootsuite report, the Google search service alone was ranked as the top website locally with over 350M visits for the month of December 2020 along with 16.5M unique users accessing the search platform alone - that’s over 43% of all users who have access to the internet in SA. Now that’s a significant portion of the online population with only one month’ worth of data.

For me, Google is a way of life – a tool that is a solution and has a significant impact on nearly all of my daily decisions, from choosing the perfect recipe to cook for dinner, to accessing my personal emails and of course searching for the nearest store that stocks that pair of sneakers I’ve been longing for. Whether it’s the Gmail platform, where I send and receive all my emails, or the Google Maps mobile app, which I am completely dependent on to know where I am, Google has a myriad of ways of collecting our data.

From some of the articles I’ve read and researched over the past couple months, Google certainly collects and stores the most amount of data on their consumers by far. I’m sure this doesn’t come as a surprise as their business model relies so heavily on collecting this data and making it simple enough for you to access on the go - from identifying your precise location when using the Google Maps app to pre-empting your browsing history when typing in the URL address bar. If it’s data, there’s a good chance that Google is collecting it.

So, just how many different types of data sources are they actually collecting?

Well, I’m sure there is infinite list which we’ll most likely never even get sight of but here are a few that you would most likely have already suspected. The data around usage reports are an obvious one to include but is certainly not limited to your IP address, crash reports, system activity, date, time, and referrer URL of your requests along with data about interactions between apps, browser and device type, app usage, carrier name, and last but certainly not least the operating system. There’s probably nothing for you to really be worried about here unless you’re doing something that you shouldn’t be doing?

But on a more personal level, they’re also collecting data on your name, phone number, payment information if you’ve made any purchases through Google, your email address and a very sensitive, contentious and questionable data source which I always believed was part of their data collection is around content in any of the emails you’ve sent and received. Just when I was writing this, right at the top of my Gmail account, I came across a notification advising me that Google is in fact not collecting my personal email content data for ‘ads purposes’… but the question remains, are they collecting it for other reasons which we’re potentially unaware of?

Well, that’s all that we know of when it comes to the collection of personal consumer data but apart from all that profile they’re building around you as a consumer, they’re also collecting and storing info about your interactions with videos, photo’s, documents and spreadsheets you’ve stored. Of course Google Search is a no brainer especially since it is such a widely used platform globally but they’re also keeping track of the videos you watch across the Google stack and the interactions you make with various pieces of content and ads and, if a third-party site uses Google services, your activity is also tracked on those sites and apps.

Google is not only tracking your browsing history if you use the Chrome browser linked to a Google account but they’re also keeping track of your Google calls including the collection and storing of called and received numbers, forwarding numbers, times and dates, call durations, routing info and the various types of calls. As far as location goes, Google keeps track of you via GPS and information that pings specific device sensors like Wi-Fi access points, cell phone towers, or Bluetooth-enabled devices. Phew…that was a mouthful!

But aside from maintaining your services to the Google stack, they really collect your data to personalise ads and content based on your specific preferences. Google also then uses that data to measure the performance of ads and then shares that data with advertisers so they can create ads that are even more effective through their targeting and tactic opportunities. That’s where our area as digital media experts really comes in.

In the conversation I had with ECR a couple weeks back, I spoke about consumers sometimes (and for me most times) ignoring T’s & C’s. I think a simple question here is when you signed up to Facebook, did you read their T’s & C’s and give your consent for them to share your data across their entire eco-system across the likes of Messenger, Instagram and Whatsapp? I’m sure if you use WhatsApp, you would have also recently received the latest notification within the app asking you to read and approve their latest privacy policy? I know I didn’t… I just hit the submit button. I find that they are quite laborious and rather difficult to read with some very high-level legal language. Sometimes we give our uninformed consent without even acknowledging what data is being used and shared across other platforms.

There’s a multitude of sensors tracking your conversations which you’ve most likely provided your consent to do already and that interconnection of sensors and tracking of conversations are key components for these major tech giants. They then use algorithms to pick up on keywords in conversation to better personalise your ad experience.

Now if you’re anything like me and do your research before making a significant purchase, you’re most likely going to consult with your family and friends (WhatsApp chats), ask your local community groups (Facebook groups), search the Google directory and then possibly go in-store before making the purchase (Google Maps). Just think about how many different data cues within each platform that you’ve just provided data to outside of the standard data collection points I spoke to earlier.

But can we stop our devices from knowing everything?

Well it’s definitely possible but it’s certainly not going to be an easy task. You would need to start by looking at all the devices you have in your home – from smart TV’s to Wi-Fi enabled gaming devices and CCTV’s… even your connected doorbell is essentially collecting your data and while you would expect these devices to be used for the intended purposes, they can sometimes be abused. Then you need to go back and read all the T’s & C’s across all devices and apps you’ve ever downloaded. That’s a big task in itself.

Obviously to remain POPI compliant, their T’s & C’s would be updated and should detail what data is being collected and of course what is being shared within their eco-systems and 3rd parties if any. Of course if you get through that long list without having consulted your legal dictionary and you don’t necessarily agree with their T’s & C’s, then don’t forget the three ‘D’ terms I spoke about right upfront…

Disable your location data and voice enabled software across all your devices (Siri, Bixby, Alexa and the like).

De-activate any connections to 3rd party apps or requests for sharing of data.

Delete any apps where you don’t agree with their collection methodologies, use of, and sharing of data.

Yes, it will most likely remind you of living through the early 90’s again but that’s unfortunately the spin off to disconnecting your data linkages to the various tech giants out there. Lastly you need to ask yourself, is the risk of your privacy and safety worth the benefits?

I’m hoping that this blog post helps in guiding your decisions going forward when downloading apps or buying new connected devices, but I speak from personal experience and I am sure you can relate that when you get a new smart device or download an app, you want to have it up and running as quickly as possible. We all crave that instant gratification and so it’s easy to race through the settings and agree to various types of data collection, sharing and storage, without thinking twice about it.

So my suggestion is really to just stop for a minute, read through and digest the T’s & C’s and then click ‘I Agree’ if of course you do…

What is a brand?

What is a brand? For some years now I've been fortunate to work on the Louis Vuitton account. It's one of the most valuable and iconic brands in the world, with a brand value of about $47.2 billion USD in 2019. After a short interlude I'm back looking after the media interests of this client again. It naturally brought me to the question of the current luxury brand landscape and the impact of the pandemic on this sector.

For some years now I've been fortunate to work on the Louis Vuitton account. It's one of the most valuable and iconic brands in the world, with a brand value of about $47.2 billion USD in 2019. After a short interlude I'm back looking after the media interests of this client again. It naturally brought me to the question of the current luxury brand landscape and the impact of the pandemic on this sector. Let’s rewind to the beginning of last year. We were living in a world of increasing information and distractions. A world where we hadn’t even really heard of Covid-19. So much has changed since then, but when it comes to attention, the fight became a whole lot tougher as distraction took a giant leap forward.

Let’s rewind to the beginning of last year. We were living in a world of increasing information and distractions. A world where we hadn’t even really heard of Covid-19. So much has changed since then, but when it comes to attention, the fight became a whole lot tougher as distraction took a giant leap forward.

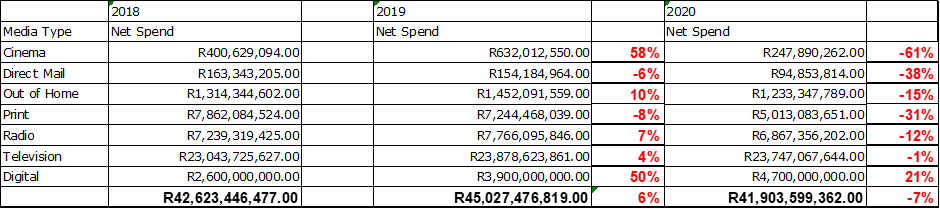

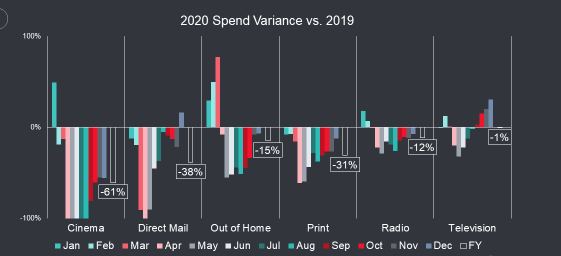

We all know that 2020 was a disruptive year due to the Covid 19 pandemic. Varying Lockdown Levels resulted in a contracted SA economy, a significant drop in advertising spend and several sectors completely shut down, not unlike what we’re experiencing now during adjusted Level 4.

We all know that 2020 was a disruptive year due to the Covid 19 pandemic. Varying Lockdown Levels resulted in a contracted SA economy, a significant drop in advertising spend and several sectors completely shut down, not unlike what we’re experiencing now during adjusted Level 4. Sources AC Nielsen and IAB

Sources AC Nielsen and IAB

By Claire Herman, Media Operations Manager at The MediaShop

By Claire Herman, Media Operations Manager at The MediaShop